Should You Buy Adobe Stock Now?

“In investing, what’s comfortable is rarely profitable.” – Robert Arnott

For more than two decades, Adobe has been one of the market’s quiet compounding machines. A 2,088% return over 24 years (14% CAGR) turned early believers into the kind of investors people envy at cocktail parties. But here’s the twist: the next decade looks less like a rocket ship and more like a steady cruise liner—powerful, profitable, but unlikely to double overnight.

And that’s not a bad thing.

Why now?

Adobe is down ~28.5% from recent highs on weak guidance. Investors are nervous about slowing growth and competition from upstarts like Canva and AI-first challengers. But that dip is what creates the opening.

If history tells us anything, it’s that moments of doubt are often when long-term compounders quietly reload.

Adobe is down 28.5% year over year!

The Business Model

Adobe, founded in 1982 and based in San Jose, is a global software powerhouse. Its bread and butter is creative tools (Photoshop, Illustrator, Acrobat), but it’s also entrenched in digital experience and enterprise workflows.

Think about it like this: Netflix for creatives More users → no extra cost → fat margins. Scalable + sticky = compounding machine.

Adobe Eco System

How They Make Money

Adobe has two main segments:

Digital Media (Creative Cloud, Document Cloud for content and documents)

Digital Experience (Experience Cloud for customer experience management).

Subscription revenue constituted 95% of total revenue in fiscal 2024

78% recurring revenue from subscriptions (Creative Cloud, Document Cloud)

High scalability: one new subscriber costs almost nothing to serve

Balance of consumer (creators, freelancers) and enterprise (marketers, businesses)

$5B+ in AI ARR proves it’s standing still.

Adobe's digital media and digital experience segments, which are their highest-performing, have shown growth. Conversely, the company's bottom three segments have been in decline.

Management & Culture

Shantanu Narayen has been CEO since 2007—an operator with staying power. He led Adobe’s pivot from boxed software to cloud subscriptions, one of the most successful transformations in tech.

Skin in the game? Management owns less than 1%. Not ideal—but Narayen’s track record and a culture of disciplined execution still carry weight.

The CEO ownership is still small as it makes 0.092% of the total shares outstanding.

Capital Allocation

Smart buys: Marketo, Frame.io expanded Adobe’s footprint

Questionable bet: The failed $20B Figma acquisition raised eyebrows (and cost $1B in termination fees)

Buybacks: $25B program through 2028—already 17% of shares queued for retirement

ROE: 36%

ROIC: 21%

Bottom line: disciplined, but not flawless.

Profitability & Financial Strength

Gross Margin: 80.3%

Net Margin: 16.4%

FCF Conversion: 142%

Interest Coverage: 50x

This is what a financial fortress looks like. Debt? Manageable, with cash to spare.

Competitive Advantage

Think of Adobe as the “operating system” for creativity. Once you’re inside its ecosystem, switching feels like ripping out muscle memory. That’s the moat: high switching costs + deep product integration.

But: Canva and AI-native tools are nipping at the edges. The real risk isn’t collapse—it’s slowly erosion of the company's ability to increase its market share and profitability.

The company seems to be responding very well to them emerging threat from AI by creating Adobe AI platform.

Adobe’s ecosystem stretches across nearly every major industry—from finance and healthcare to retail and high-tech—embedding its tools so deeply into customer workflows that it has become the digital backbone of how businesses create, engage, and operate.

Valuation

Trading at 22x earnings and FCF

Market pricing in ~12% FCF growth over the next decade

Historical FCF growth: 22% CAGR (though only 10% in the last 2 years)

Call it fairly valued. Not a screaming bargain, not frothy either.

Market Potential

Adobe plays in a $293B addressable market by 2027. Its revenue? Just $21.5B. That’s less than 11% share. Add in AI-driven Firefly, freemium products (Express, Acrobat AI Assistant), and enterprise adoption—and the runway is long.

Adobe is uniquely positioned to capitalise on the explosive growth of generative AI and digital content, having built on a decade of AI innovation. The company is empowering creators by putting the power of AI in their hands, doing so responsibly.

Source: Adobe

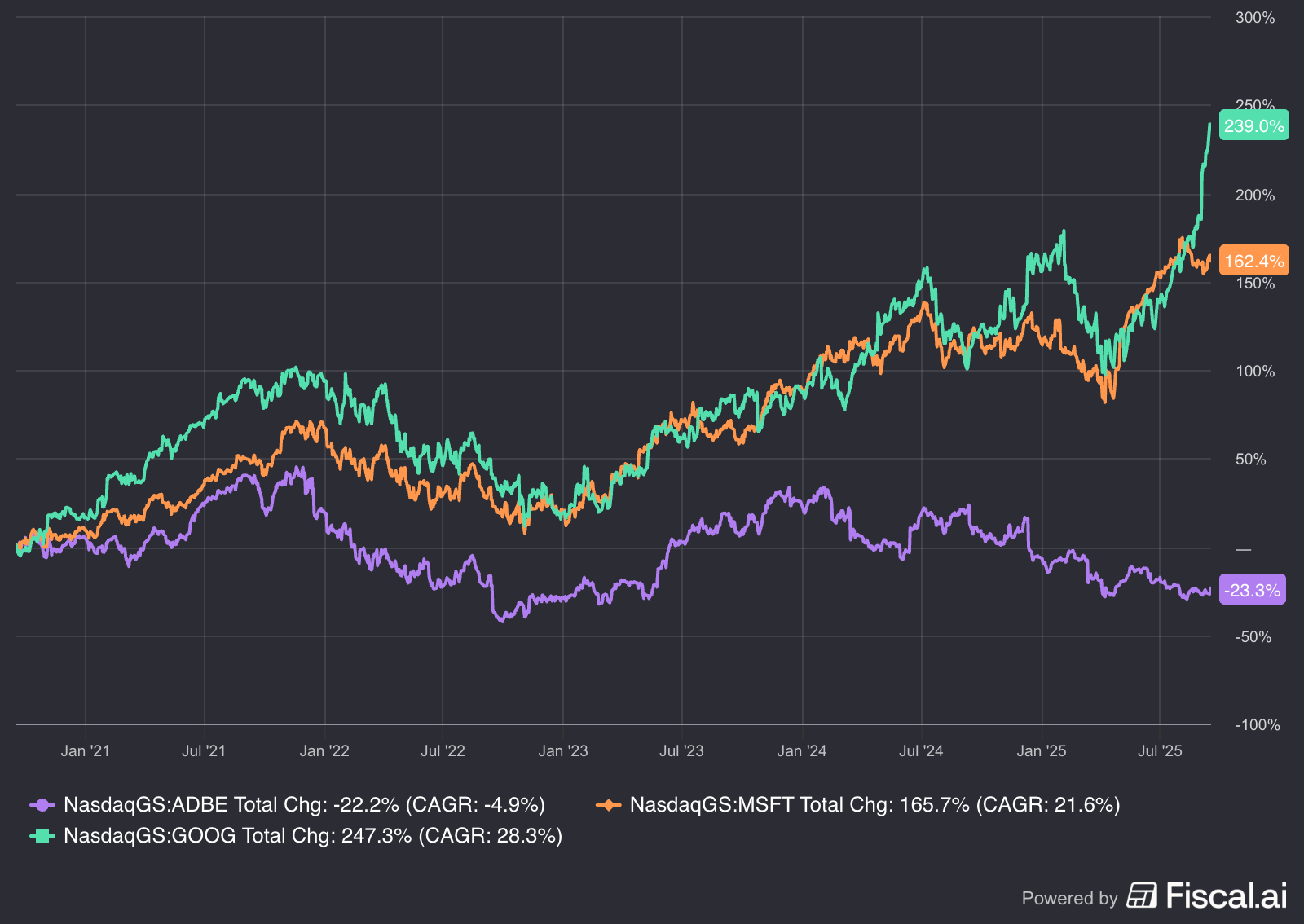

Performance vs. Peers

23-year CAGR: 15.2%

Last 5 years: only 4% CAGR—momentum has cooled

By contrast, Microsoft and Alphabet kept compounding faster

Adobe feels less like a Tesla, more like a Johnson & Johnson: dependable, durable, but with a speed governor.

Key Risks

Competition: Canva, AI challengers

Capital allocation missteps: another “Figma moment” would sting

Regulation & churn: subscription fatigue, customer frustration over cancellations

Innovation risk: fail to lead in AI, lose relevance fast

Slowing growth vs historic 20+CAGR

Conclusion

Only 2% of stocks created $75 trillion in net wealth. Adobe is one of them.

Will the next 10 years mirror the past 20? Probably not. But in a world chasing shiny new objects, there’s something comforting—and profitable—about a cash-rich, high-margin giant quietly buying back shares and embedding itself deeper into the digital fabric.

Sometimes the best investments aren’t rockets. They’re compasses.

But the next decade looks more like moderate growth for Adobe than explosive upside.

At silvercrosscapital.com, we built the Outlier Portfolio on one truth: a handful of stocks create nearly all long-term wealth.

Adobe already did it.

Our mission? Find the next Adobe before Wall St. does.