Anthropic Is Winning the AI War — But Should You Still Buy the Stock?

Let’s talk about Anthropic—not with Wall Street buzzwords, but with an investor’s eye on durable growth and strategic edge." This isn’t just another “foundation model company with strong ARR growth and expanding compute spend.” Nope. This is an AI research lab turned ultra-ambitious platform firm with deep philosophical roots and a frontier-safety mindset. It’s selling Claude-powered intelligence to governments, corporations, and cloud titans—and doing so on its own terms.

It’s a high-margin, defensible platform company riding the heart of the AI-industrial revolution. With runaway revenue growth, strong backing from Big Tech, and a vision for safe AGI, the case for Anthropic as a generational AI powerhouse is gaining steam.

But at what cost?

How They Make Money

source: Taptwicedigital.com

Anthropic operates on a usage-based, cloud-integrated model, monetizing Claude through:

API usage via AWS Bedrock, Google Cloud, and direct contracts

Enterprise platform deployments (ClaudeOps)

Custom model training for strategic partners

Long-term R&D & safety grants from government and institutional partners

Their commercial GTM is lean but potent. Most growth comes from deep partner integrations (Amazon, Google, Notion, Slack) rather than brute-force sales.

The Claude 3 family (Opus, Sonnet, Haiku) has made Claude the most context-aware and safety-optimized model on the market.

And yes, revenue is increasingly recurring, with retention rates over 135% in the enterprise segment. This is sticky intelligence.

Management

Source: Alex Kantrowitz - Medium

Co-founder and CEO Dario Amodei isn’t your typical startup founder. A former OpenAI researcher, he left to build a different kind of AI company—one focused on constitutional safety, interpretability, and alignment-first AGI.

Amodei doesn’t posture on earnings calls or court meme stock status. Instead, he builds. Quietly. Relentlessly.

Anthropic’s culture is rigorously research-driven, values-aligned, and deliberate. Their internal alignment charter reads more like a philosophical doctrine than a startup handbook.

They hire fewer engineers, but demand uncommon alignment of intellect, mission, and long-term thinking. No sales bros. No hype cycles. Just builders, aligned on the safe scaling of intelligence.

Growth at Blistering Speed

Revenue trajectory: Anthropic’s revenue has soared from ~$10M in 2022 to $1B in 2024, and is projected to reach $2.2B in 2025—a ~120% year-over-year rise.

Annualized revenue milestone: By May 2025, Anthropic’s annualized revenue hit $3B, up from $1B in December 2024—a speed rarely seen in SaaS history

Source: Taptwicedigital.com

Market Position & Scale Metrics

Generative AI market share: Anthropic holds about 3.91%, trailing behind OpenAI at ~17%

Claude monthly active users: Peaked at 18.8M in late 2024; now down to around 16M users as of early 2025.

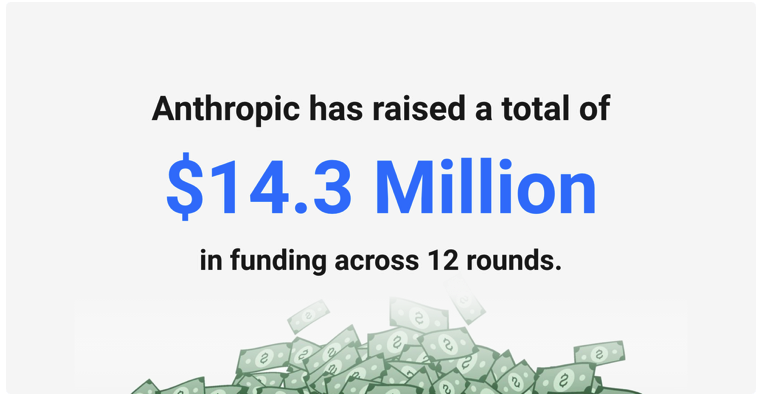

Valuation & Funding:

Post-money valuation stood at $61.5B as of early 2025.

Total funding raised: $14.3B, with backing from Amazon ($8B committed), Google (~$2B), Lightspeed…

Team: Approximately 1,097 employees in 2025

Business Model & Competitive Moat

Anthropic is monetizing Claude via:

Enterprise API usage (via AWS, Google, Databricks) with token-based pricing

Premium Claude‑enterprise deployments, custom model training, and safety research contracts

Its competitive advantages include

Claude’s massive 200K+ token context window

Constitutional AI base—alignment-first architecture

Deep integration in cloud platforms (AWS, Google Cloud)

Stickier enterprise deals versus consumer users

Why Investors Should Care

Fastest-growing SaaS-like trajectory: Multiple investors note Anthropic’s sprint from $1B to $3B ARR within ~6 months as unprecedented.

Revenue forecasts: Anthropic projects up to $34.5B in revenue by 2027; more conservative estimates suggest $12B—implying massive growth expectations!

Valuation runway: Discussion is already underway to raise a new round valuing the company at $150B+

Risk Category

Key Considerations:

Valuation

Currently trading at ~$60B–61.5B; pricing in future dominance

Execution

Scaling Claude at enterprise-speed, maintaining model leadership

Competition

OpenAI, Google Gemini, Meta, Mistral all ramping up aggressively

Dependency

Heavy reliance on Amazon & Google partnerships/credits

Regulatory Risks

AI safety scrutiny, public-benefit corporation structure

Financials

Still burning cash—burn rate forecast ~ $3B/year; expected break-even by 2027!

Investor Takeaways

Anthropic is not just growing fast—it’s executing a strategy that blends philosophical rigor, enterprise uptake, and deep alignment focus.

Key financials show a company moving from bespoke research to scalable business model and predictable enterprise cash flow.

But at a ~$60B+ valuation already pricing in future dominance, investors should weigh “what if they’re right?”against what if execution falters or competition accelerates?

Bottom Line:

Growth profile: Explosive

Strategic moat: Well-defined

Financial discipline: Improving, but not yet profitable

Valuation: Aggressive—only fits if Claude becomes foundational global infrastructure

SCC Rating: 75%

Anthropic is priced for transcendence. Any hiccup could disappoint. Investors should tread carefully and manage expectations—reality has a hard time competing with revolution.

Take Your Investments to the Next Level

We deliver deep, narrative-driven insights on the companies shaping tomorrow’s world. Track the AI frontier with us.

Risk Disclosure: This summary uses third‑party data for information only. It is not investment advice. Always consult a licensed financial advisor before making investment decisions.